There is more

Related news

No items found.

Electric cars tend to dominate the headlines, but what about the 40-ton trucks that transport goods across our economy? Although heavy-duty trucks make up less than 2% of vehicles on the road in Europe, they produce roughly a quarter of road transport CO₂ emissions. Therefore, decarbonising freight is imperative for meeting climate targets. However, the transition to electric trucks (eTrucks) is still in its early stages: as of 2021, 96% of EU trucks were still diesel-powered, with only 0.1% being zero-emission. Electric heavy-duty trucks are emerging as a crucial frontier in the transition to zero-emission mobility. However, unlike passenger EVs, electrifying freight requires a far more complex ecosystem of stakeholders, infrastructure and operational changes. This article examines what makes eTrucks unique within the EV landscape, and identifies the most promising and scalable opportunities, particularly in asset-light, software-driven areas that could accelerate adoption.

Early-stage adoption and rapid growth

Global sales of medium- and heavy-duty electric trucks reached approximately 90,000 units in 2024, almost doubling from the previous year and accounting for almost 2% of all new truck sales worldwide. Adoption remains uneven across regions, but the trend is clear: early-stage deployments are now expanding, particularly for short-haul and vocational applications where charging and duty cycles are already feasible.

This unit growth translates into substantial market value projections. Globally, the eTrucks market is estimated to be worth around $15-20 billion in 2024 and is expected to grow to approximately $120-150B by 2030, implying a robust CAGR of 30-40%, as deployments shift from initial pilot schemes to large-scale fleet purchases. Europe is following a similar trajectory from a smaller base, at around $3-5B in 2024, but is rising rapidly toward $20-30B by 2030, reflecting an even steeper CAGR of 40-50% through to the end of the decade.

Policy is a major accelerator: the EU mandates require that approximately one-third of new trucks sold in 2030 be zero-emission. Consequently, all major forecasts predict significant growth, expecting 20-30% of new trucks globally to be electric by 2030. Although regulation provides a structural push, near-term adoption remains highly sensitive to incentives. Early-stage fleet demand still depends on purchase support and toll/road charge relief. Recent pauses or cuts to schemes such as Germany’s e-truck subsidies have demonstrated how quickly order momentum can soften when incentives change. Therefore, the market will be policy-sensitive until TCO parity is achieved and maintained.

What are the top 3 bottlenecks slowing eTruck adoption?

Charging infrastructure gap

The Charging infrastructure gap is arguably the biggest hurdle slowing eTruck adoption. Currently, public charging for heavy-duty vehicles is woefully inadequate, creating a classic "chicken-and-egg problem": fleets are reluctant to purchase electric trucks if they cannot reliably charge them, while investors hesitate to build expensive truck stops until more eTrucks are on the road. This lack of infrastructure, comparable in severity across Europe and North America (where most fast chargers are designed for cars), poses an urgent challenge for long-haul operations.

The magnitude of the required infrastructure build-out is significant:

Estimates of the required capex are similarly large: McKinsey projects that around €7 billion of charging-infrastructure investment is needed in Europe by 2030 (excluding major grid upgrades), rising to approximately €40 billion by 2040 as public corridors and depots scale.

Beyond public networks, there is the challenge of depot charging. While 80-85% of eTruck charging is expected to occur at private depots or fleet hubs by 2030, scaling this infrastructure is difficult because many logistics yards lack the necessary power capacity or space for high-speed chargers.

Policymakers and industry are responding: the EU’s Alternative Fuels Infrastructure Regulation (AFIR) mandates at least one 350 kW+ charger every 60 km on core highways by 2025. The EU has provided a budget of €1 billion for 2024-2025 and has already allocated over €2.5 billion in grants for alternative fuels infrastructure including megawatt truck charging, since 2021. Furthermore, major European truck OEMs have jointly committed €500 million (Milence) to develop a heavy-vehicle charging network. However, coverage must increase dramatically to instill confidence in operators.

.avif)

Figure 1: Projected public charging infrastructure in selected European markets, 2020-2030

High vehicle costs and economics

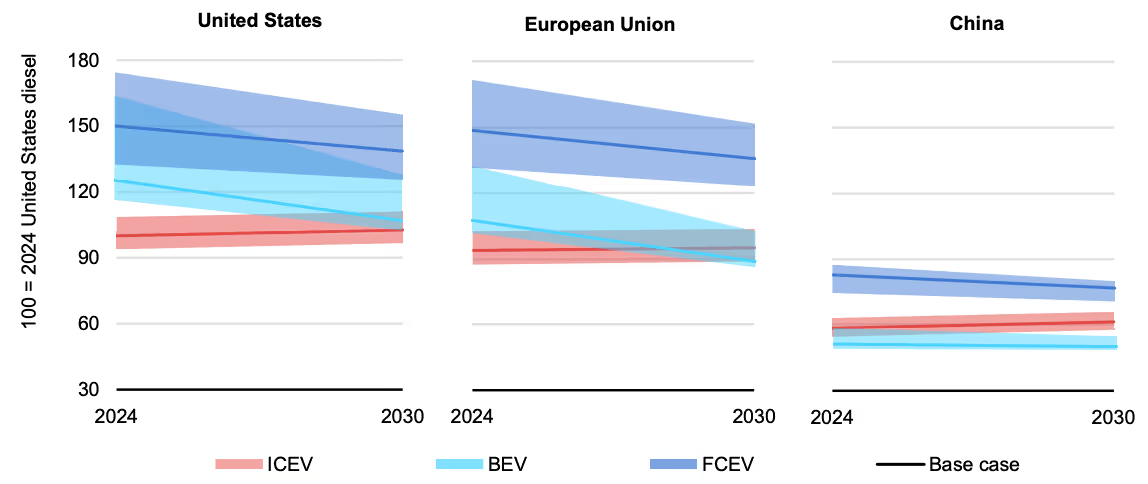

The bottleneck related to high vehicle costs and economics is a major factor slowing fleet adoption, as the Total Cost of Ownership (TCO) for electric trucks is often higher than that of diesel trucks. This economic uncertainty is critical because heavy transport generally runs on thin margins, making companies hesitant to invest.

The core of the economic challenge is the high initial purchase price:

Figure 2: Total cost of ownership for diesel, battery electric and fuel cell heavy-duty trucks, 2024-2030

Notes: ICEV = internal combustion engine vehicle (diesel truck); BEV = battery electric vehicle; FCEV = fuel cell electric vehicle.

Manufacturers are working to address this, with plans to halve eTruck prices by 2030 as battery costs continue to fall (35% in EU). In the meantime, government intervention and innovative strategies are bridging the financial gap:figure

These combined factors are expected to enable electric trucks to become cost-competitive with diesel in many segments in the next 5 years.

Grid constraints and energy demand

The bottleneck concerning grid constraints and energy demand arises because charging heavy trucks requires an enormous amount of power, for which much of the current electrical infrastructure was never designed. A single 1 MW truck charger can consume as much electricity as 750 homes. If a fleet attempts unmanaged charging simultaneously, there is a risk of overloading a local substation.

The grid bottleneck is driven by several factors:

To address these power access issues, innovative solutions are crucial. Some charging hubs utilize large battery buffers to draw power slowly from the grid while allowing trucks to charge quickly. Furthermore, smart energy management systems can stagger or modulate charging (e.g., scheduling charging sequentially or overnight instead of all at 6 pm), effectively reducing peak loads and avoiding costly infrastructure upgrades.

Nevertheless, until grids are reinforced and smarter distribution methods are fully implemented, access to power remains a critical bottleneck for the eTruck rollout. Proactive planning is essential to ensure major freight corridors have the required electrical capacity.

Distributed Energy Resources (DERs)

The large battery packs required by electric trucks, which often range from 500 to 800 kWh, mean that these vehicles can be considered powerful distributed energy resources (DERs). Moving beyond simple consumption, the strategic management of eTruck charging - particularly through vehicle-to-grid (V2G) technology - is crucial for balancing the energy system. This flexibility creates significant business opportunities for fleet operators, enabling them to participate in grid services such as demand response and transform depots into “virtual power plants”. This creates an additional revenue stream and helps fleets to avoid steep utility peak demand charges, which could otherwise negate any operational cost savings. At a system level, the potential impact is immense: utilising eTrucks as flexible storage could save European grid operators an estimated €4 billion per year in avoided infrastructure and operating costs by 2030. By absorbing excess solar or wind energy and discharging it during peak times, V2G technology can help to mitigate grid capacity constraints and enable the integration of up to 40% more solar PV capacity into the network. Ultimately, this capability accelerates the shift towards a smarter, more flexible energy system.

The role of software platforms and key innovators driving electric freight

Software solutions are playing a crucial, asset-light role in accelerating the eTruck transition by providing scalable platforms designed to bridge the major bottlenecks identified in the heavy-duty vehicle sector. These companies can be grouped into scalable categories that target operational efficiency, energy management, and high capital costs across the eTruck value chain, while often spanning multiple areas of impact rather than fitting neatly into a single one.

I. Smart charging, grid integration and energy management

These companies offer pure-play software platforms that enable fleet and depot operators to balance, prioritize, and stagger charging sessions automatically, maximizing the use of existing grid capacity and avoiding steep utility demand charges. These platforms effectively turn EV fleets into sophisticated Distributed Energy Resources (DERs).

II. Route optimization, interoperability and access

These solutions streamline access to charging infrastructure, simplify payments, and ensure fleet operations remain efficient by minimizing range anxiety and downtime.

III. Fleet planning, TCO optimization and asset analytics

These software platforms maximize utilization and minimize operating expenses by providing fleet managers with critical data and planning capabilities, thereby accelerating the timeline for electric trucks to achieve TCO parity.

IV. Foundational software and infrastructure enablement

These companies provide underlying software or planning tools that accelerate the deployment and ensure the technical viability of the charging ecosystem.

Several infrastructure companies are also developing software for the wider ecosystem. Notable examples include Milence, which offers digital charging and network services, E.ON Drive Infrastructure (EDRI), which provides a platform and fleet-facing solutions, and IONITY Fleet, which provides corporate fleets with network access, centralised billing and management tools.

Unlocking the freight potential

Decarbonizing heavy-duty transport is a non-negotiable imperative for achieving global climate targets, given trucks’ outsized share of road CO₂ emissions. The eTruck market is still early and relatively small, but momentum is real: pilots are becoming commercial rollouts, and a first generation of specialists is raising meaningful capital to scale. Although significant funding has already been raised globally ($4.9 billion across 2023-2024 for EV charging startups as well as some recent announcements, such as Delta Charge, NexDash and EcoG), fleets continue to face the same hard bottlenecks.

The massive, instantaneous power demands of heavy vehicles strain existing grids, depot capacity is often insufficient, upgrade timelines are long, and demand charges plus high upfront costs keep Total Cost of Ownership (TCO) uncertain and operational risk elevated.

The successful, scalable rollout of electric fleets depends not primarily on infrastructure quantity, but on advanced software orchestration. Innovative, asset-light platforms focusing on smart charging and energy management are the crucial solutions necessary to maximize existing grid capacity and bridge the economic TCO gap, making constrained infrastructure usable at scale.

Ultimately, the electrification of freight offers a significant opportunity: by converting heavy-duty eTrucks into sophisticated Distributed Energy Resources (DERs), the sector can evolve from merely consuming energy to actively participating in grid balancing, thereby accelerating the essential transition towards a smarter, more flexible energy system. Whilst early in its development, we believe in the potential of the (software) market opportunity.