Physical AI: when intelligence leaves the screen

How AI is entering factories, warehouses, and construction sites, and where 4impact capital sees the software investment opportunity. Written by Sophie Millenaar and Hadin Alkatiri.

AI has conquered the digital world: text, code, images, video. But until recently, it lived behind screens. That is changing. AI is entering the physical world in factories, warehouses, construction sites and critical infrastructure. The Physical AI market is projected to grow to over €430 billion by 2030. For impact investors, this shift matters enormously. Only 5% of firms say Physical AI is currently transforming their organisation, but 41% expect it will within three years. Physical AI has the potential to slash industrial emissions, protect workers from harm, and address Europe’s deepening labour crisis, all while building defensible, scalable software businesses.

But the opportunity also demands intellectual honesty. A model achieving 95% accuracy in the lab may drop to 60% in deployment, because the physical world introduces variability no simulation can fully capture. Humanoid robots doing backflips make for great content; a robot that fails 100 times a day on a warehouse floor creates more work than it saves. The sim-to-real gap, multi-modal data complexity, and the need for continuous data curation remain genuine barriers.

This article provides an introduction to Physical AI, sets out how we at 4impact capital define it, why we believe the timing is right, and where we see the most compelling intersection of impact and returns.

Perceive, Reason, Act

Our Definition of Physical AI

The term Physical AI is used loosely. NVIDIA’s Jensen Huang frames it as AI models that understand the real world and plan actions for robotics. a16z defines it more broadly as deployable systems built for the real world, grounded in new operating models, industrial infrastructure, and defensible data collection.

At 4impact capital, we apply the following definition: Physical AI is an AI system that closes the loop with the physical world. It perceives physical data, reasons about it, and triggers a real-world action or decision.

A camera on a production line detects a crack. The AI classifies it, distinguishing a defect from dirt. The system triggers rejection. That is Physical AI: perceive, reason, act. By contrast, a warehouse climate system that lowers the temperature when a sensor crosses a threshold is not, it follows a preset rule with no reasoning. That distinction between intelligence and automation is important.

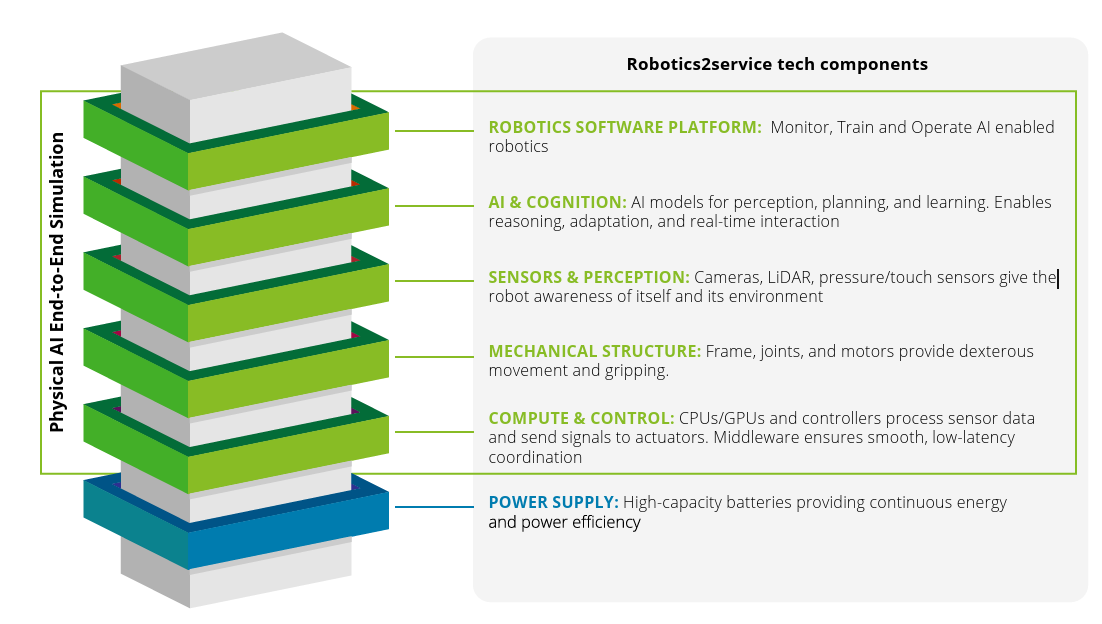

Figure 1: The Technology Layers of Physical AI (Deloitte, 2026)

This definition is also our filter. We include companies building robotics software, autonomous systems, vision-based quality control, fleet orchestration, and drone operations software. From our definition we exclude passive analytics dashboards, general BI tools and sensor-only systems without a reasoning layer

Why the Timing Is Right

Hardware costs collapsed. IP cameras cost under €50. LiDAR is down over 90%. Barclays estimates humanoid robot unit costs have fallen roughly 30x in a decade, from ~$3M to ~$100K. Bank of America projects material costs reaching $13,000–$17,000 within a decade.

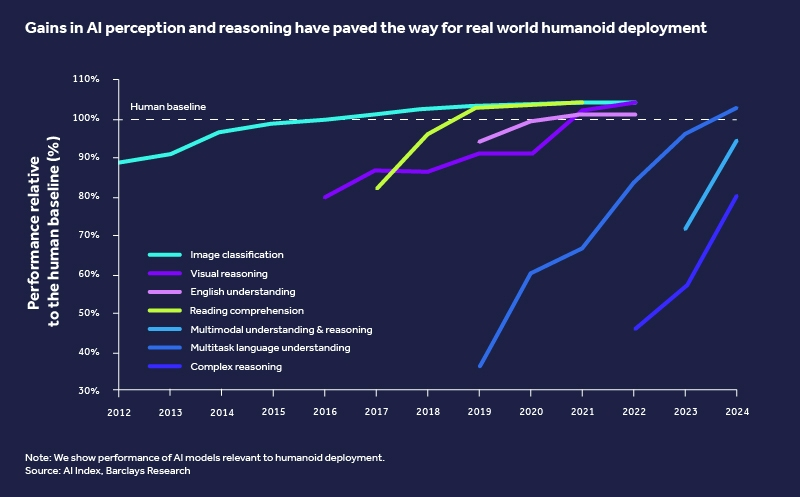

Models got radically more efficient. The "densing law" was found, which states that LLM capability density doubles approximately every 3.5 months (Nature, 2025). This means equivalent model performance can be achieved with exponentially fewer parameters over time. Inference costs fell 280x (Stanford HAI, 2025). Robotics Foundation Model (general-purpose “brains” like Google DeepMind’s Gemini Robotics and NVIDIA’s GR00T) now enable a single model to transfer across different robots and tasks. Vision-Language-Action (VLA) models enable robots to follow natural-language instructions and generalise across environments.

Figure 2: AI Perception and Reasoning Ability (Barclays, 2026)

Europe’s labour crisis is structural. Germany projects a shortage of 7 million skilled workers by 2035, with 700,000 positions currently unfilled in construction, healthcare, and engineering (EURES, 2024). There are 2.7 billion deskless workers globally, 80% of the workforce, receiving roughly 1% of enterprise software spend (Emergence Capital, 2018). 53% of these workers report burnout; 43% are at risk of quitting (BCG, 2022). 54% of European employers expect shortages to worsen over the next five years (WEF, 2025).

Capital is pouring in. Global robotics venture capital totalled approximately $27.6 billion across 1,000+ deals in 2025 (PitchBook, 2026), out of which $5.8 billion in Q4 with $840 million going to robotics software & AI. In Europe, robotics VC doubled to €1.45B, and the European Commission committed €1.3B through its Digital Europe Programme for 2025–2027.

Why This Matters to an Impact Investor. At 4Impact capital, every investment must contribute to our two impact pillars: Good for Planet or Good for People. Our Fund II is classified under SFDR Article 9: we exclusively invest in digital startups with an environmental or social objective, where impact is in lockstep with the business model. That means we look for companies where every unit of revenue corresponds to a measurable outcome. Physical AI sits squarely at this intersection through emissions reduced, waste eliminated, or workers protected.

The software opportunity: sectors and companies

The hardware is the body; the software is the brain. And the brain is where impact compounds. As software-first investors, we look for companies that sit on commodity hardware and build proprietary intelligence on top. When we examine which industries have the most software-first impact Physical AI companies emerging in Europe, three stand out.

Industrial Manufacturing

Cutting Emissions at the Source

Industry accounts for approximately 23% of global CO₂ emissions, with around 70% generated along supply chains (Yin, 2025). AI-driven process optimisation is delivering material reductions: peer-reviewed research shows AI frameworks achieving 18–20% reductions in industrial energy consumption and CO₂ output through real-time scheduling, defect detection, and waste heat recovery. Predictive maintenance alone cuts unplanned downtime 30–40%, directly reducing the energy wasted on start-stop operations.

We are tracking a growing wave of European startups building this intelligence layer, amongst which:

Deltia.ai (Germany) uses computer vision on existing factory cameras to digitise manual assembly processes. The system perceives assembly steps via video, reasons about deviations from the standard process, and triggers alerts or line adjustments in real time. This delivers up to 20% productivity gains and reduces rework and material waste. Pure software, running on commodity cameras.

Forgis (Switzerland) is building a “cognitive factory” software platform for adaptive process control. The system ingests real-time sensor and machine data, reasons about process deviations, and autonomously adjusts production parameters to optimise yield and energy consumption. Early pilots shows configuration times reduced up to 60%, downtime reduced by 30%, and throughput increased by 20%.

Sereact (Germany) has built Vision-Language-Action Models that give any robot the ability to perceive objects, reason about how to grasp and manipulate them, and execute pick-and-place tasks all without manual programming or retraining. The system handles unknown items on day one, adapts grip and trajectory in real time when items shift, and flags anomalies before placement.

Construction & Infrastructure

Saving Lives and Decarbonising the Built Environment

Construction is Europe’s deadliest major industry. Over 700 fatal incidents occur annually, driven by falls, collapses, and equipment failure (Automation in Construction, 2024). The sector’s productivity grew at just 0.4% annually from 2000–2022, far behind manufacturing’s 3.0% (McKinsey, 2025). AI-powered computer vision is shifting safety from reactive to proactive: organisations deploying AI-based monitoring report up to 20% reductions in safety incidents (Deloitte, 2025), and autonomous robotics can reduce worker exposure to hazardous tasks by up to 72% (Fulcrum, 2025).

Monumental (Netherlands) combines AI-driven robotics with site intelligence to address labour shortages through precision bricklaying. Their robots perceive the construction environment, reason about placement precision against architectural plans, and execute masonry work autonomously on real sites.

Baubot (Austria) develops mobile construction robots that automate labor-intensive tasks on building sites, addressing workforce shortages through intelligent on-site execution. Their robots integrate advanced sensing, navigation, and task-specific tooling to operate safely in dynamic environments, enabling precise and efficient processes such as drilling, marking, and material handling directly from digital construction plans.

Warehouse & Logistics:

Orchestrating Efficiency, Reducing Emissions

Logistics robots now account for 52% of all professional service robots installed globally (IFR, 2025). The European warehouse automation market is projected to reach $27 billion by 2033 at 18.5% CAGR (Market Data Forecast, 2025). The key insight: in warehouse automation, the differentiator is not the robot, it is the orchestration software. Mixed-fleet environments require an intelligence layer coordinating heterogeneous machines and humans in real time. Integration and orchestration determine automation success (McKinsey, 2024; Logistics Viewpoints, 2026).

Olivaw (Germany) builds a vendor-agnostic robot fleet orchestration platform. The software perceives real-time warehouse conditions across mixed robot fleets, reasons about optimal routing and task allocation, and dynamically re-deploys robots to minimise idle time and energy waste.

Pyck (Germany) develops an open-source, AI-native warehouse management framework. Their platform modularizes complex warehouse processes into adaptable components, allowing teams to design, optimize, and scale operations with full control over workflows, data, and costs while leveraging AI to automate configuration and continuously improve efficiency.

SyncroBot (Germany) orchestrates heterogeneous AMR fleets, optimising throughput while cutting congestion and energy use across warehouse operations.

How We Evaluate

Physical AI Technology Through an Impact Lens

Rather than cataloguing technologies, we evaluate them against our Impact Assessment Framework. Each must address a significant problem, deliver measurable outcomes, and demonstrate that impact scales with revenue:

Vision-based quality control and inspection replaces manual inspection on production lines and construction sites. The impact case: every defect caught before it becomes scrap avoids wasted materials and the embodied energy that produced them. In our own portfolio, Tvarit AI solutions can reduce defects in Metal manufacturing by up to 60%.

Fleet orchestration and multi-robot coordination manages mixed fleets of robots and humans in real time. The impact case: optimised routing reduces robot energy consumption and eliminates the need for facility expansion. Amazon’s integration of AI-orchestrated robotic fleets across next-generation fulfilment centres has delivered 25% faster delivery and a 25% boost in overall efficiency.

Predictive maintenance and process optimisation anticipates failure and optimises industrial processes. The impact case: preventing unplanned downtime avoids the energy-intensive start-stop cycles that generate waste heat and emissions and process optimization reduces energy consumption. In our own portfolio, Myrspoven’s AI-driven energy optimisation achieves a 20% average energy savings rate per building.

Autonomous inspection and safety monitoring uses computer vision, robotics, and drones for real-time hazard detection, infrastructure inspection, and PPE compliance. The impact case: directly protects human life and prevents emissions from undetected leaks. Amazon sites integrating robotics have seen a 15% reduction in incident rates as employees transition into oversight and diagnostics roles.

Europe’s Distinctive Advantage

Europe holds a unique position in this landscape. Decades of industrial legacy data from world-class engineering and manufacturing create a moat that cannot be replicated by software alone (EY, 2025). As one industry leader put it: the United States leads in large language models and hyperscalers, but Europe has legacy data: decades of experience in high-quality engineering, manufacturing, and industrial operations. Training AI on this data is Europe’s opportunity and unique selling point.

European manufacturing generates €2.5 trillion in value added and operates with high robot density. The regulatory environment, including the EU AI Act (entering force in 2026) and CSRD, is creating compliance-driven demand for exactly the kind of AI-powered monitoring and reporting that Physical AI companies provide. The EU’s €200 billion InvestAI initiative, including €20 billion for AI gigafactories and continued commitments through the Digital Europe Programme, signals that public capital is now aligned with the sector’s trajectory.

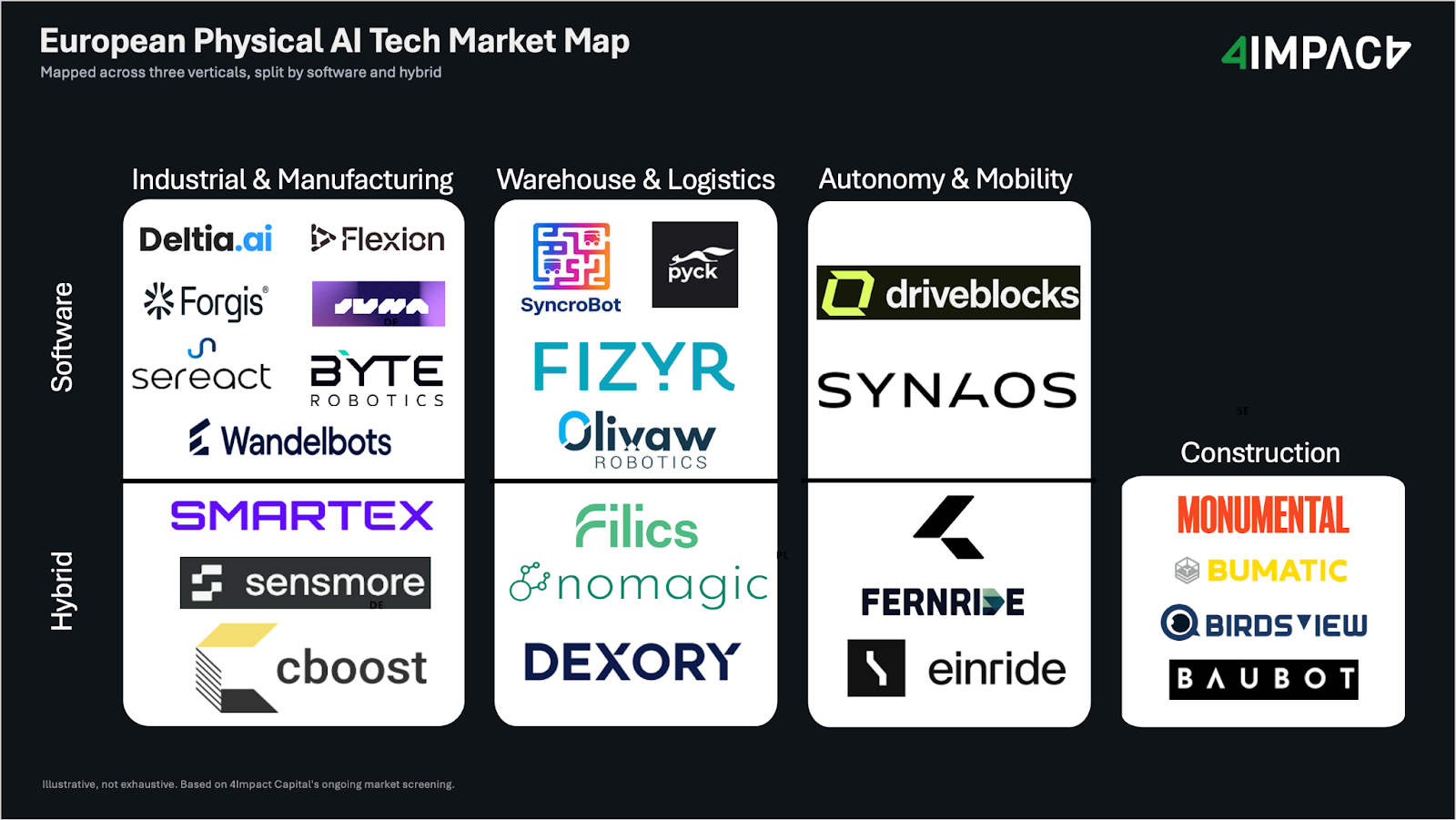

Figure 3: European Physical AI Market Map

Where This Leaves Us

Physical AI is attracting enormous attention. But there remains a persistent chasm between lab demos and production-ready systems. The companies that will win are not the ones building the most advanced hardware, but the ones developing the most intelligent software at the fastest pace. Software that survives contact with the messy, variable, unforgiving physical world.

At 4impact capital, we are actively looking for founders building this intelligence layer. Companies where impact and business model are in lockstep: where every unit of revenue corresponds to positive impact. If your software reduces emissions, prevents injuries, or eliminates waste as a core function of your product, we want to hear from you.

Which companies did we miss in our research? And which sector within Physical AI should we do a deep dive on? Let us know.